One topic that comes up a lot in parenting/FIRE circles is this all-consuming idea that we should start socking away money in a college fund so that the little one can go to school debt-free. While on the face of it this impulse is admirable why wouldn’t you want your kid to have a debt-free college experience? If they graduate without a load of debt on their backs they will be free to just leap off into the working world and start raking in the cash from the great job they got because of their degree.

That is one possible future but what's equally as likely is that instead of getting a more realistic degree like mechanical engineering they instead followed an interest in the poetry of 14th and 15th Spain. While that grounding in poetry makes them a great storyteller and engaging conversationalist it's probably a bit harder to find gainful employment with that degree.

So, on one hand, saving money for their college worked out great and they are off to a great start on the other hand you just shoved a lot of money down a hole it may never come out of. When you are looking down at that baby in your arms can you honestly say to yourself that you know for sure that saving money in a fund dedicated to higher education is not going to blow up in your face.

The answer is NO… in case you're wondering. No one can possibly predict what another human being is going to do tomorrow much less in 18 years. That's why I along with my partner have no intention of saving for college for our kid. As far as we are concerned what they do when they turn 18 and are adults is up to them. If they want to go to college it's up to them to figure out how they are going to pay for it. I know this position is not a popular one but I would like the chance to make a few arguments defending this position before anyone just assumes we are awful parents who should lose custody. Reason 1- We’re Selfish I will just get the selfish reason out of the way first. If you have read anything I have in the Frugal Living Library then you have probably figured out that we are on the path to FIRE or FIFE (Financial Independence Freedom Early) as I like to call it. If we were to put enough money in a college account to pay for all of the little one’s college we would severely damage our ability to save for our future on the timeline we want. We are not willing to mortgage our future on the vague idea that the kid will need money to go to school. To be blunt, paying for college is their problem. Reason 2- They need to reap what they sow Some of the best lessons I have learned in my life stem from the times I have made mistakes. Some of those mistakes were minor, others not so much but I always took away something useful from those mistakes. Now some parents think it is their job to protect their children from everything that might hurt them. But when you don’t expose living things to adversity they never grow strong or resistant to the bad things that life can throw at them. Everything needs to suffer a little bit so when the big challenge comes that can handle it. How this applies to the college fund is that going into college debt can teach you more about money than any personal finance class could. My kid will have two options to pay for college they can,

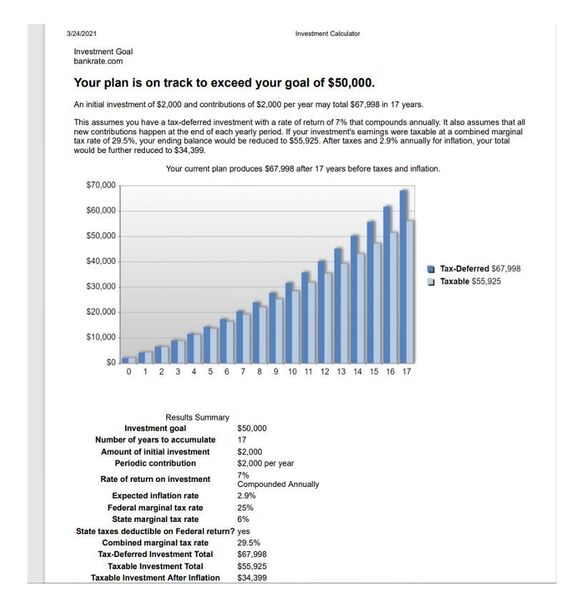

Either way is good in my mind because both will teach discipline, forward-thinking/planning and make them feel the financial weight of their choices. I learned things about myself and how to manage money that I never considered before I was confronted with paying off my college loans. Reason 3- Financial Discipline/Credit Score Just to be clear I plan on making sure that my kid has a much firmer grasp of money and personal finance than I did when I went to college. But that knowledge will be all theoretical till they actually have to manage their money and tackle a mountain of student loans after they graduate. Nothing teaches you to manage money better than knowing you have thousands of dollars of debt breathing down your neck and influencing all your financial choices. Paying off student loan debt will not only be good for their internal discipline but it will also give them a better financial footing in the outside world. My student debt was my first dip in the credit system and by the end of paying it off, I had a great credit score for twenty-five-year-old. That credit score set me up to get a great rate on a house mortgage a few years after I paid off college. My partner on the other hand was lucky enough to get a full ride to college so they graduated debt-free. This is good but the dark side to that debt-free college was the complete lack of credit. They did not exist in the world of loans so when we bought a house together they couldn't be on the mortgage because it jacked up our rate. They struggled for years to get enough of a credit history to be able to access a decent loan rate. Reason 4- No Flexibility While the goal of plans like a 529 college fund is admirable and the tax advantages of the account are nice, the utter lack of flexibility is anathema to me. You can use a 529 plan for one thing and that is paying for education. But going back to where I started this post you have no clue what that baby in your arms will want to do in 18 years. Maybe they will want to go to college, maybe they will join a trade or maybe they are a budding entrepreneur and they already have a business idea or an online business waiting in the wings for more time or money. Or maybe heaven forbid they just want to get a job right away and rise in the ranks from there. The point being is you don’t know so why would you put money in such a limiting place if you don’t have to. The rest of the story…. Hopefully, by now you have realized by now that my partner and I are not horrible parents and we really do want the best for our child. We just don't think that doing everything for our kid is the best way to teach them life's important lessons. Sometimes you have to crash and burn before you really understand that the choice you made was a poor one. That being said I do believe that putting some money away for your kids future is a good thing. I just don’t think a college fund is the way to do it. Just as food for thought consider the following. Right now the government gives you a 2,000 dollar tax credit per year just for having a kid. If you were to take that money and stick it in a standard brokerage account it could look something like this by the time they are 18. Just in case you couldn't read it, it says that the account could be worth 67,998 dollars by the time they are 18. That is money that could be used for starting a business, buying a house or just seed money for moving to where the job is. This approach is much more flexible than a standard college fund and if you want it could still be used to pay for college. I hope I gave you something to think about. Sources https://www.sec.gov/reportspubs/investor-publications/investorpubsintro529htm.html

0 Comments

Leave a Reply. |